One effect of the emergence of cryptocurrency is that it has made a lot of people rethink our relationship with currency generally, and with the big banking institutions.

For example, in June 2018, Switzerland held a “sovereign money” referendum in which Swiss citizens rejected by a ratio of three to one a proposal to end fractional reserve banking and give sole money-creation authority to the Swiss National Bank. Cryptocurrency wasn’t mentioned in the proposals, but it was on many people’s minds during this vote.

Why? Because the fact that cryptocurrency exists means that there is a very real possibility that global economies will “disintermediate banks from money” as Michael J. Casey suggests, and he also claims that the leaders of this change will not be the activists one typically associates with bitcoin and other crypto assets, it will be the central banks themselves.

They will initiate the move towards a true “money of the people”, because they will have to in order to “remain relevant in a post-crisis, post-trust, digitally connected global economy.”

A non-governmental currency

This might be an anarchist’s dream situation, but for those who want money removed from government control, the move to digital currencies will encourage more competition worldwide by opening the door more non-governmental digital currencies. Plus, when smart contracts are used to manage exchange rate volatility, it is likely that we will find that the people and businesses involved in international trade will no longer need to rely on the dollar, Euro or British pound as the cross-border currencies of choice.

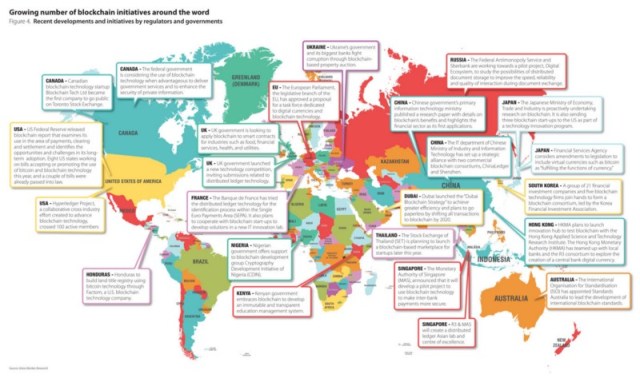

There hasn’t been much enthusiasm for a central bank-issued digital currency (CBDC), largely because the banks didn’t really like the idea. The Bank of England has done research into the concept, but BoE governor, Mark Carney then warned about financial instability if his bank supplied digital wallets to every citizen, because this would then give the man in the street the same right as regulated commercial banks to hold reserves at a national bank.

Inefficient banks

Basically, traditional banks are the problem and not just for cryptocurrencies; they are inefficient with respect to fiat money as well. Their technical, social and regulatory infrastructure is past its sell by date and it’s a costly system. Banks maintain centralised, non-interoperable databases on outdated, mainframes. They rely on multiple intermediaries to process payments, plus ledgers that have to be reconciled against each other using time-consuming fraud-prevention mechanisms.

Banking solutions

There are solutions though: one is to gradually introduce CBDC stating with non-bank financial institutions and cascading it down through corporations and smaller business to individuals. A central bank set CBDC interest rate would also help and could be part of managing the money supply. It is more likely that this will happen first in the developing world where there is a greater need and appetite for something like a fiat digital currency that offers protection from inflation. In the developed world, the banks may take longer to get their heads around the concept of moving away from decades old systems, but they will have to respond somehow, because the crypto genie is out of the bottle.