Neobanks, or digital banks, arrived in Australia in 2018, dues to a change in legislation, and since then there has been a flurry of activity. Some might even call it a tsunami of neobanks, and this has led to a high level of competition in the country’s banking sector, something that hasn’t occurred for decades.

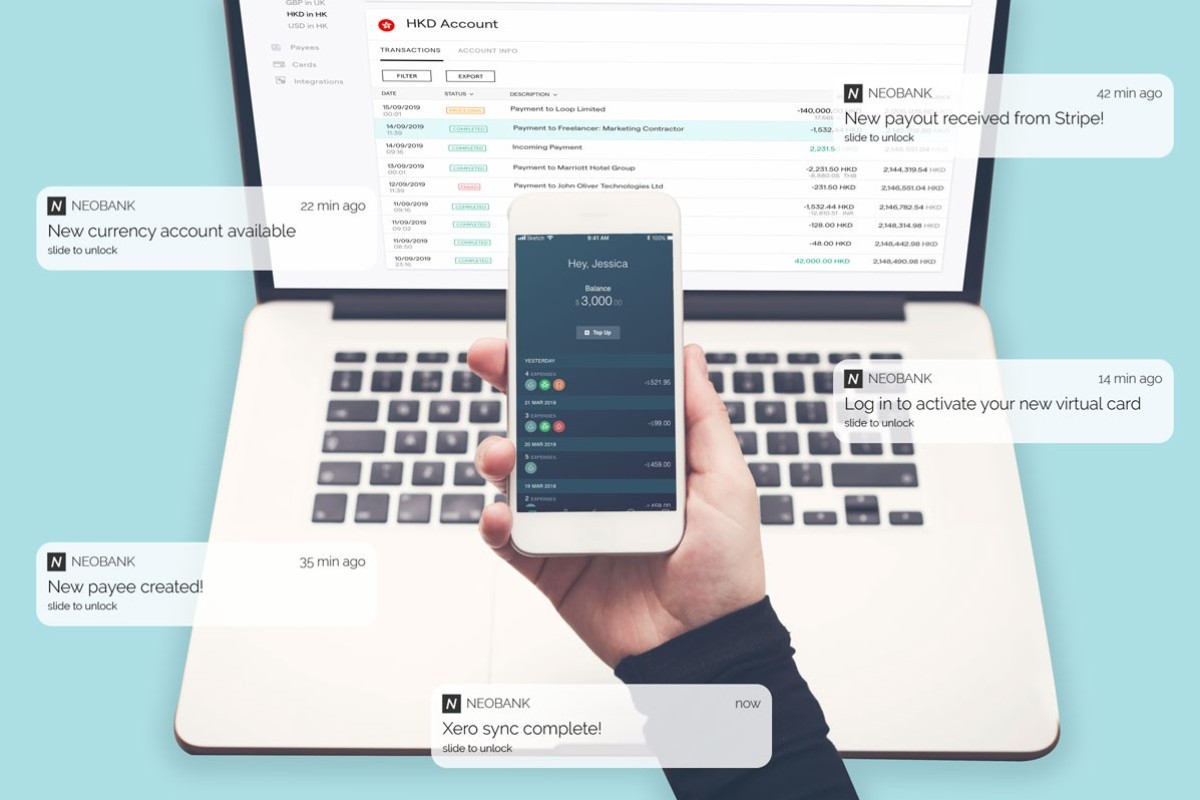

The neobanks are app-based banks accessed mostly from a smartphone. They don’t have physical branches and they promise clients a ‘touch of the button’ 24/7 service, and most of them have much lower charges than the traditional banks.

Neobanks have been growing in popularity outside Australia for some time, with Europe being a leader, especially the UK. As Jack Derwin points out, the fact that they are doing so well in the UK, and a number of them are registered there, such as Starling, Revolut and Monzo, is a good sign for Australia.

The digital banks are a more recent addition to the Australian banking scene, because until legislation changed in 2017/18, it was extremely difficult to start a neobank. Whilst the previous legislation was intended to protect the consumer, it was perhaps too restrictive, and anti-competition.

In 2017, Scott Morrison, who then headed the Treasury, dramatically simplified the application process to enter the banking sector. As a result, within months neobanks were lining up to enter the market.

Still, entering the banking sector is never easy. Neobanks need a banking licence, a core banking system and a substantial fund of money: one neobank founder told Business Insider Australia that $100 million was the figure needed to start up.

It takes time to raise that kind of money, and to get a banking licence, which can take up to 12 months, as the newcomer must convince the financial regulator to trust the product.

So, what is the advantage to using a neobank? Unlike traditional banks, they are more cost efficient. They don’t have a network of offices and the fact they have lower overheads, means they can pass the cost saving onto the client. Also neobanks have access to the best tech and can therefore optimise their product. It only takes minutes to set up an account, compared with all the paperwork needed for a bank. So, the consumer appeal is there, combined with free accounts and lower charges.

As Derwin says, “From recognising higher than usual bills, notifying you of unused subscriptions, and even helping you switch to a cheaper energy provider, neobanks say they can do banking better.”

That might not be hard to achieve in Australia, where the traditional banks have admitted to extorting fees for non-existent services, to the point they were even charging dead people. They also admitted to lying to the regulators, holding forged documents, failed to verify customers’ expenses when approving loans, and sold insurance to people who couldn’t afford it. And as Derwin says, with four banks controlling 80% of Australia’s business, there was no incentive for them to do better.

All this adds up to a reason for Australians to love neobanking. They now have around five to choose from, including Volt and Xinja, and the UK’s Revolut is testing the market. This is definitely a geographical space to watch for anyone interested in neobanks.