Banking is going through some changes thanks to the arrival of neobanks. The traditional banks continue to work at their own pace, and are still largely bound by legacy systems that go back decades. Change is not a simple process for them: it is similar to trying to change the direction of a massive oil tanker at speed on the high seas. In other words it is something that takes a while.

The arrival of the neobanks, which are the digital-only challenger banks, (there are challenger banks that don’t fit in the neobank niche because they are more like traditional banks) has caused an upset in the banking sector, but what is the real difference between a neobank account and the type of bank account that most of us already have?

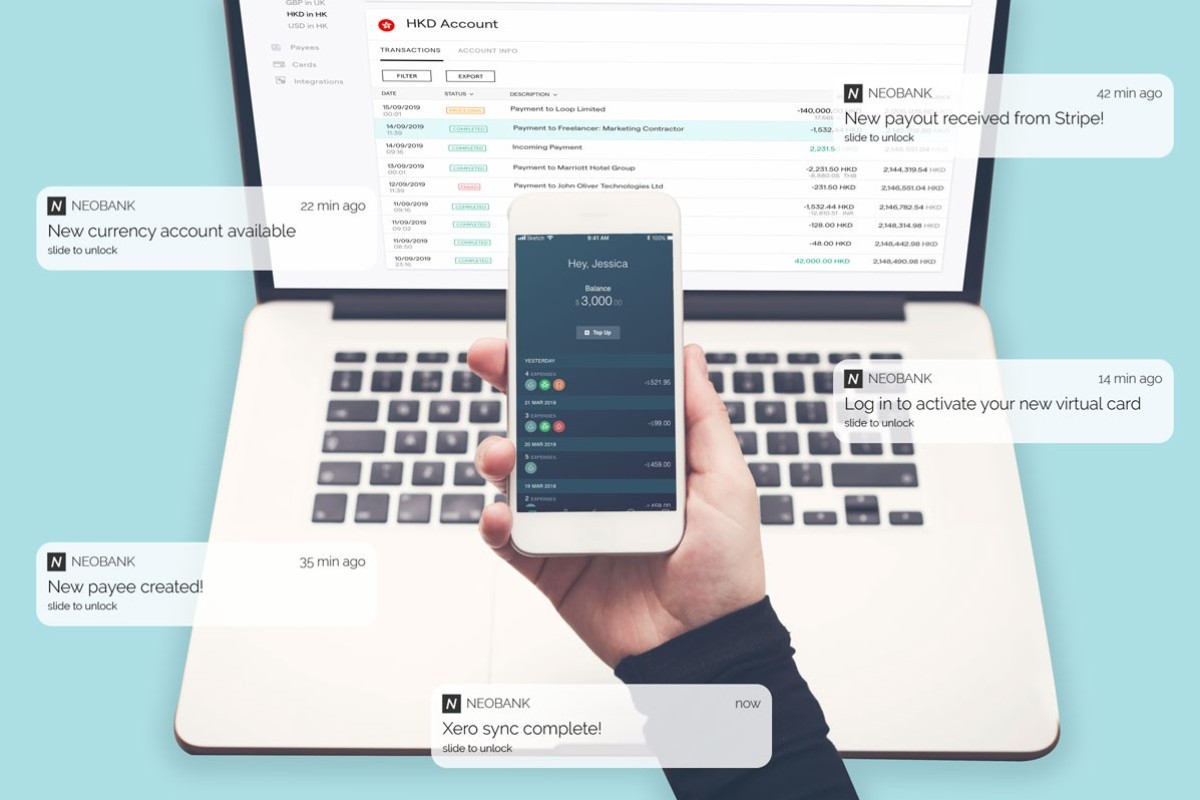

The first, and most basic difference is that they are technology driven. And they don’t have physical branches. That can be off-putting to customers who feel more secure by having a branch that they can go to and talk to someone. In this way, neobanks have a greater appeal to younger sections of the population who are used to operating their existing bank account through an app and online.

Often neobanks don’t have a full banking licence, but they can still offer the range of services offered by traditional banks. They can do this because they have an alternative type of financial services licence, such as an e-money licence, or they have partnerships with financial service providers that hold an appropriate licence.

Opening a neobank account is extremely simple and can be done via a smartphone, or a computer in minutes. There’s no wait while all your documents are assessed by head office. This has a huge appeal for many customers, especially those people who may be dismissed by traditional banks, because they don’t have a large enough income to make them a ‘worthwhile’ customer. Some banks now insist that customers keep the balance in their account at a certain level, and this means many people are excluded from holding an account, or find that their account is suddenly closed.

And we all know that traditional banks often charge exorbitant fees. The neobanks offer free accounts, as well as a range of accounts with a monthly fee, but even these are much lower than an established bank would charge for the same service. Chime, for example, is a neobank in the US that offers debit cards and fee-free overdrafts.

Neobanks are also cutting out a sector for themselves with small businesses and freelancers, which is a sector that the traditional banks don’t serve very well. For example, UK neobank Coconut focuses on serving freelancers. They’ve developed specific accounting features, including VAT and invoicing that cater to the day-to-day needs of the self-employed. For example, a freelancer who needs to request payment from a client can use Coconut to send invoices directly from the app.

Overall, neobanks are changing the entire banking experience. It will take some more time to grow this new financial sector, but it seems to me that every day one meets yet another person who has added a digital-only banking service to the tools they use to manage their money, and that is progress.